401k plans are a scam anyway, as it’s locked up to be used by the bankers, and you’ll pay a high penalty to take out your money early except for a couple reasons. You’d be better off just paying your taxes and investing it yourself, as you’re allowed to use so much a year without having to pay any capital gains taxes on it once you retire. But this does show that people are struggling, and after credit cards have hit new highs, people are going for their 401k accounts to get by. But will the Iran war and the blow to energy and shipping set off the financial collapse?

A capital gains rate of 0% applies if your taxable income is less than or equal to:

- $48,350 for single and married filing separately;

- $96,700 for married filing jointly and qualifying surviving spouse; and

- $64,750 for head of household.

A capital gains rate of 15% applies if your taxable income is:

- more than $48,350 but less than or equal to $533,400 for single;

- more than $48,350 but less than or equal to $300,000 for married filing separately;

- more than $96,700 but less than or equal to $600,050 for married filing jointly and qualifying surviving spouse; and

- more than $64,750 but less than or equal to $566,700 for head of household.

https://www.zerohedge.com/markets/americans-are-plundering-their-401k-savings-record-numbers

By Tyler Durden

More Americans are tapping their retirement savings to deal with financial emergencies, according to the Wall Street Journal.

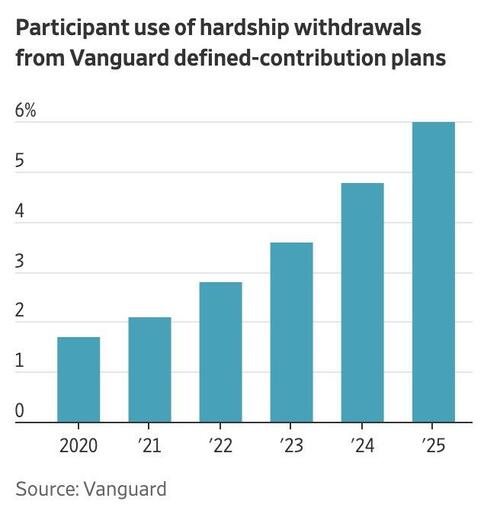

Last year, a record 6% of workers in 401(k) plans administered by Vanguard took hardship withdrawals, up from 4.8% in 2024 and about 2% before the pandemic. The figures point to a mixed financial picture: many Americans are doing well, but a growing share are under pressure.

At the same time, retirement balances have climbed alongside strong markets, and more workers are participating in 401(k) plans. As a result, those accounts are increasingly becoming a financial backstop when unexpected expenses arise.

Hardship withdrawals have now increased for six straight years. Part of the rise dates back to a 2018 change that made it easier to access retirement funds by removing the requirement that workers take a 401(k) loan before requesting a hardship distribution. Vanguard administers plans for nearly five million participants.

The most common reasons for withdrawals last year were avoiding foreclosure or eviction and covering medical costs. The median amount taken out was $1,900.

Financial strain is also showing up in other ways. More Americans are falling behind on some types of debt, including mortgages, while credit-counseling groups report that the average income of people seeking help has increased. Even so, unemployment remains relatively low and consumer spending has stayed resilient.

Policy changes have also expanded the situations where hardship withdrawals are allowed. A 2022 law gave employers the option to permit withdrawals for victims of domestic abuse and people impacted by federally declared disasters. It also allows workers to withdraw up to $1,000 penalty-free for an emergency once every three years, with the option to access funds again sooner if the money is repaid.

Another driver is the spread of automatic enrollment. As more employers automatically place workers into retirement plans unless they opt out, more people now have savings available to draw from during emergencies.

The Journal writes that among about 1,300 employer plans Vanguard administers, 61% automatically enrolled new hires in 2025, up from 34% in 2013.

Workers who take hardship withdrawals from traditional accounts typically owe income tax and may face a 10% penalty if they are under 59½.

Despite the rise in withdrawals, overall retirement savings remain strong. The average 401(k) balance rose 13% in 2025 to a record $167,970.

Participation is also growing. A record 45% of workers increased their savings rate in 2025, matching the share that did so the year before, largely through automatic escalation programs.

“People are saving more, remaining invested, and being automatically rebalanced in a professional way,” said David Stinnett, head of strategic retirement consulting at Vanguard.