(Headline article below) I’ve always thought 401k accounts are a scam when you look at penalties for early withdrawal, fees to the OCGFC investment firms managing them, and just how difficult it is for you to take out your money if you evem can (they even force you to take money out at a certain age whether you need it or not, so they can tax it). And this was big business putting the burden of retirement on your shoulders instead of managing a pension fund which has more regulations. Now the big financial firms with trillions under management want to use those trillions in 401k accounts to increase their profits at the expense of regular working men and women. Consequently, at the wife’s jobs over the years, she’s had coworkers that have seen their 401k accounts dip by six figures as the markets tank, because many people are just not savvy enough to manage a 401k account, or go by faulty guidance from the management firm looking for a higher return.

However, some experts caution that this move could pose greater risks to retail investors, as private equity firms may attempt to offload underperforming assets.

And this Heritage Foundation is an OCGFC operation that does not have your best interests in mind, and were even involved in trying to harm the Republicans in the last election with Project 2025, which became a Demonrat talking point.

Others argue that such concerns are overblown, including Heritage Foundation Chief Economist E.J. Antoni, who said he “doesn’t see any evidence” to support the notion that “private equity is going to be able to offload this junk to unsuspecting consumers.”

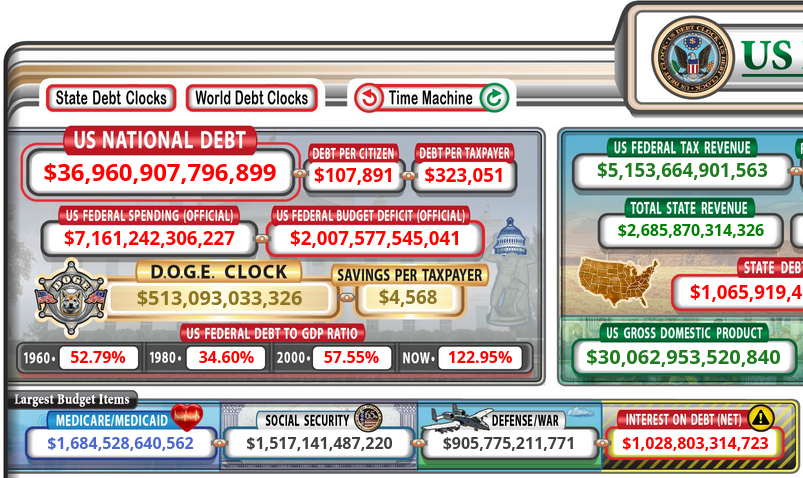

Consequently, the bigger threat to your 401k account is the federal government which has been salivating over these trillions of dollars, as they’d like to grab them with a promise to pay you later while they pay down the debt (be stolen more likely). And our national debt is pretty scary, at $323,051 per taxpayer. And look at how we’re spending over $1 trillion to service the debt now, more than military spending.

https://dailycaller.com/2025/06/05/private-equitys-next-frontier-your-retirement-savings/

By Melissa O’Rourke

As fundraising dries up and past investments come under pressure, private equity firms are vying for access to the trillions of dollars that everyday Americans hold in their 401(k)s to help fill the gap.

In recent months, private equity firms have been lobbying the Trump administration to clarify some legal guidance that limits private equity’s reach into the retirement system. However, some experts warn that such a change would mean average American consumers using their retirement savings to essentially bail out private equity shops that are in growing need of liquidity.

“The fear is that private equity will use retail money to dump the companies that they can’t get rid of,” Eric Salzman, who has worked in the financial sector for over 35 years as a regulator, trader, consultant and risk manager, explained to the Daily Caller News Foundation. “You’ll probably have inappropriate investments going to an investor base that does not belong in that product.”

Private equity firms own businesses across many sectors, including healthcare, which has raised concerns about viewing institutions such as hospitals as mere financial assets. They are now seeking to gain access to the roughly $9 trillion in 401(k) plans held by about 35% of working-age Americans, which have traditionally contained publicly traded stocks and bonds.

I’m done letting private equity treat Pennsylvania hospitals like a piggybank they can empty out and smash on the floor.

It’s time for us to stand up for our local hospitals and nursing facilities and put in place real safeguards against private equity. Pennsylvania families —… pic.twitter.com/jg8QtQvyhj

— Governor Josh Shapiro (@GovernorShapiro) May 15, 2025

Private equity firms pool funds from large institutional investors, such as pension funds and endowments, as well as ultra-high net worth individuals, to invest in private companies. These firms typically take an active role in managing the companies with the goal of improving their profitability to eventually sell, distributing the profits from the sale to both the investors and the fund manager.

In addition to the capital raised from investors, private equity firms use high amounts of debt to finance their deals, known as leveraged buyouts. This business model thrived during the years of low interest rates, but rising borrowing costs and growing market volatility have made it harder for firms to strike new deals, exit old ones and return capital to investors, causing a steep drop in fundraising.

“What you have now is that this model doesn’t work anymore. They aren’t generating enough cash to meet debt payments, and many of these guys are starting to default,” explained Salzman.

This dynamic has made the trillions of dollars held in Americans’ 401(k) accounts an increasingly attractive target. Still, some say incorporating private equity into retirement plans poses serious risks for everyday investors as these investments are generally less liquid, charge higher fees and are harder to value than traditional options like stocks or bonds.

In 2020, the Department of Labor (DOL) under the Trump administration issued guidance allowing private equity investments to be a part of certain diversified portfolios, such as target-date funds. Under the Biden administration, however, DOL reversed course, saying such private equity investments are not “generally appropriate for a typical 401(k) plan.”

Just days before President Trump’s inauguration, top private equity managers like Blackstone and UBS held a meeting to discuss strategies for obtaining Washington’s support in accessing individual investors’ retirement plans, Bloomberg reported.

There are signs that the Trump administration is listening. Administration officials are considering an executive order or presidential memo to ease the legal concerns keeping private equity from most workers’ 401(k)s, Bloomberg reported in May.

Historically, private equity returns have outperformed investment options available to the average consumer. Private equity delivered average annual returns of 13.1% over 25 years, compared to 8.6% from the S&P 500, according to a 2024 analysis from Cambridge Associates.

Advocates say allowing private equity investments in retirement accounts will allow consumers to benefit from the high returns they have offered in the past and diversify their portfolios.

“For decades, pension funds across America have invested in private assets because they deliver the strongest returns for retirees. Adding private assets as an investment option is a smart, safe way to diversify retirement accounts and help Americans save more for their futures,” a spokesperson for the American Investment Council, a leading private equity interest group, told the Daily Caller News Foundation.

However, some experts caution that this move could pose greater risks to retail investors, as private equity firms may attempt to offload underperforming assets.

“Your average person just takes the default premixed 401(k) portfolio, so they could buy into something they don’t really understand. And if they want to take their money out and there’s too much private equity, you’re going to have a problem,” said Salzman. “Generally, retail does not get the best deals. The private equity managers and the big institutional managers keep the best stuff for themselves.”

Salzman is not alone in this view.

“Retail could end up saving these companies that people cannot sell,” Orlando Bravo, who manages a private equity investment firm, recently told the Financial Times. “The retail investor might not be as sophisticated. There might be more risk of them not understanding what they’re involved in, and this could create all sorts of problems.”

Even if the Trump administration relaxes the rules surrounding private investments in retirement accounts, it remains unclear whether plan sponsors will actually adopt them due to high fees and the fact that they cannot be easily bought and sold.

“Some plan sponsors are very much against this initiative to make direct investments to private equity available through the defined contribution plan,” Bridget Bearden, research and development strategist at the Employee Benefit Research Institute, told CNBC. “They think that it’s pretty illiquid and very risky, and don’t really see the return for it.”

Others argue that such concerns are overblown, including Heritage Foundation Chief Economist E.J. Antoni, who said he “doesn’t see any evidence” to support the notion that “private equity is going to be able to offload this junk to unsuspecting consumers.”

“If these private equity investments were really as bad as the opponents say, why would anyone invest in them? This is the free market; if something is a bad investment, it will go south, and people will stop investing in it,” he told the DCNF. “We don’t want bureaucrats to dictate to consumers what they can or can’t invest in or how they should or shouldn’t be saving for retirement, or anything else for that matter.”

Salzman agreed that investors have a right to make their own decisions but emphasized that there must be “some guardrails because time and time again, retail investors have been clobbered, ripped off, sold products that are not suitable — could be outright scams — and there needs to be some sort of protection.”

The White House, Treasury Department, Securities and Exchange Commission and DOL did not respond to the DCNF’s requests for comment.